How much is NZ Super? All about New Zealand Superannuation

![]() Reading time: 6 minutes

Reading time: 6 minutes

What’s NZ Super? How much is it?

New Zealand Superannuation is the state pension paid to Kiwis aged 65 and older.

You can take NZ Super into account when you're planning for retirement. The current rates below give a broad idea of how much it is this year. Could you live on that? If not, it’s time to put some other plans in place to bridge the gap between what it provides and what you’ll need to fund your lifestyle after stepping back from paid work.

About the author

Standard NZ Super rates as of 1 April 2026

Here are the current superannuation rates after tax has been deducted at rate 'M' (the standard code if NZ Super is your primary income). For other tax codes, see the Work and Income website.

Standard NZ Super rates (after tax, code M)

|

Single: living alone |

||

|---|---|---|

| WEEKLY $555 |

FORTNIGHTLY $1110 |

ANNUALLY $28,868 |

|

Single: sharing |

||

|---|---|---|

| WEEKLY $512 |

FORTNIGHTLY $1025 |

ANNUALLY $26,647 |

|

Married, civil union or de facto couple: one partner qualifies and the other is not included (ie, you’re 65+ and qualify, but your partner is under 65 or doesn’t meet the requirements and doesn’t need financial support from your NZ Super) |

||

|---|---|---|

| WEEKLY $427 |

FORTNIGHTLY $854 |

ANNUALLY $22,206 |

|

Married, civil union or de facto couple: both partners qualify (ie, both of you are 65+, either citizens or residents, and meet residency rules) |

||

|---|---|---|

| WEEKLY $854 |

FORTNIGHTLY $1708 |

ANNUALLY $44,412 |

|

Married, civil union or de facto couple: one partner qualifies and the other is included (ie, you’re 65+ and qualify, and your partner doesn’t qualify but depends on your NZ Super) |

||

|---|---|---|

| WEEKLY $812 |

FORTNIGHTLY $1624 |

ANNUALLY $42,227 |

Source: Ministry of Social Development

The level of NZ Super payments is set by the government each year, which reviews and adjusts them to take into account any increases in the cost of living (inflation) and average wages.

The after-tax NZ Super rate for couples (who both qualify) is based on 66% of the ‘average ordinary time wage’ after tax. For single people, the after-tax NZ superannuation rate is close to 40% of that average wage.

NZ Super is paid fortnightly every second Tuesday. If that falls on a holiday, the payment is processed earlier. Here’s where to see the dates.

If you have income from another source (if you’re still working or earn investment income), your after-tax amount of NZ Super may differ. You can find out exactly what you’re entitled to from Work and Income by calling 0800 552 002 (you’ll need to have your IRD number handy) or their website. See Inland Revenue’s website for more information as well.

Who’s eligible for NZ Super?

All eligible New Zealanders receive NZ Super, regardless of how much they:

- Earn through paid work

- Have in savings or investments

- Have by way of other assets

- Have paid in taxes.

To be eligible for NZ Super, you need to be aged 65 or over and a legal resident of New Zealand. You can get NZ Super even if you’re still working.

Currently, you need to have lived here for 10 years since age 20. Since July 2024, however, this residency requirement has been gradually increasing to 20 years by July 2042.

You’ll need to have lived in New Zealand, the Cook Islands, Niue or Tokelau (or a combination of these) for 20 years since age 20, with five of those years from age 50 or older.

What does it mean to ‘have lived in New Zealand’?

To have lived in New Zealand means you were both a resident and physically present in the country at the same time.

What ‘resident’ means

Being resident means you permanently made your home in New Zealand for the required number of years.

For example, if someone usually lives overseas, but visits New Zealand from time to time, those visits do not count as time in which they are resident and present, because they’re not permanently making their home here.

What ‘physically present’ means

You will need to be physically in New Zealand for the required number of years. If you left, you weren't physically present in New Zealand for that time period.

For example, if someone usually lives in New Zealand but takes overseas holidays, those holidays do not count as time in which they are resident and present (even if they are employed and paying tax in New Zealand), because they are not physically here.

Here’s more information on the change to the residency requirement.

Here’s more information about NZ Super eligibility.

It’s important to remember that NZ Super may be different in years to come in terms of who gets it and when.

Overseas pensions can affect NZ Super

If you receive a pension from another country (such as UK state pension, Australian Age Pension, or similar), this may reduce your NZ Super payment by the amount you receive from overseas.

For more information, call Work and Income on 0800 777 227 or email international.services@msd.govt.nz.

How to apply for NZ Super

If you’re eligible, you can apply for NZ Super three months before you turn 65. There’s a form on the Work and Income website, or Work and Income can be reached on 0800 552 002.

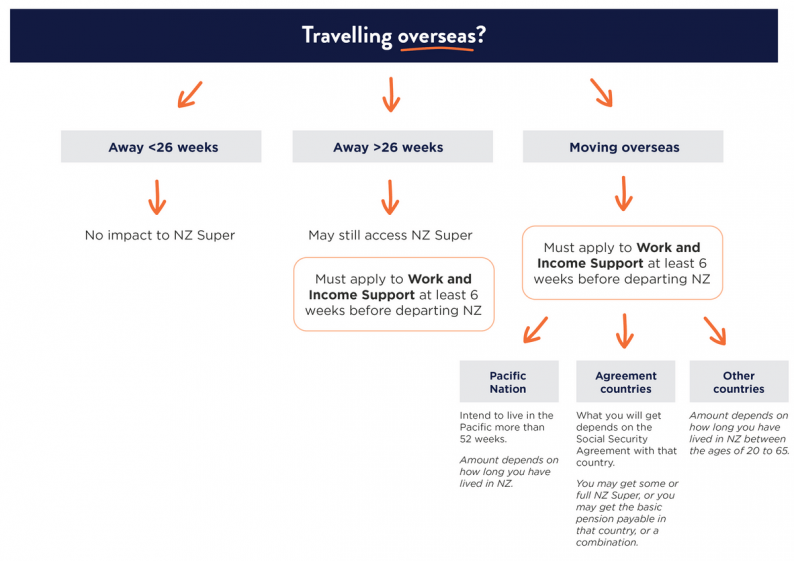

Can you still get NZ Super if you’re heading overseas?

Probably. Being away from New Zealand for less than 26 weeks is generally fine. If you’re away for longer than that or you’re moving away permanently, the amount you receive could be less than you would get if you stayed in New Zealand, and will depend on which country you’re in.

You should consider taking advice from Work and Income’s International Services before making decisions, particularly if NZ Super is a big part of your retirement income.

For more details on receiving NZ Super while travelling or moving overseas, see this Te Ara Ahunga Ora Retirement Commission document and the Work and Income website.

Will NZ Super be enough to live on?

NZ Super is generous by international standards, but it only goes so far. Many of us will have a gap between what it provides and the retirement lifestyle we’re hoping to achieve.

To understand how much your gap might be, you can plug your numbers into our retirement calculator.

About the author

You may also like...

Guide

How to plan, save and invest for retirement

Ask anyone who's retired, and they will say to start saving for retirement as soon as you can! Even if…

Guide

Find housing options in retirement

As you get older and your needs change, where you decide to live can shift as well. Knowing your options…

Guide

When you’re thinking of living in a retirement village

Moving into a retirement village can be a great option to live out your later years. But with so many…

Guide

Four approaches to spending in retirement

Discover four expert-backed rules of thumb for retirement spending that help balance enjoyment and security.

Guide

Manage your money in retirement

Life after you stop working can mean living without a steady income, so you’ll have some choices to make. This…

Video

How to future-proof your retirement village choice

Moving into a retirement village is a big decision, so it’s important to be clear about your circumstances and lifestyle…

Video

The price of retirement village living

Buying into a retirement village isn’t an investment, it’s an expense. For a smooth transition and a financially secure future,…

Video

How retirement villages work

Navigating the financial and legal aspects of moving into a retirement village can feel daunting, but if you get good…

Visit us on social

© Office of the Retirement Commissioner